ASTS is either the most important telecom company of the decade — or a very expensive failure.

The company connecting 2.8 billion smartphones directly to satellites. Here's the full picture — technology, partners, competition, and what I'm actually watching.

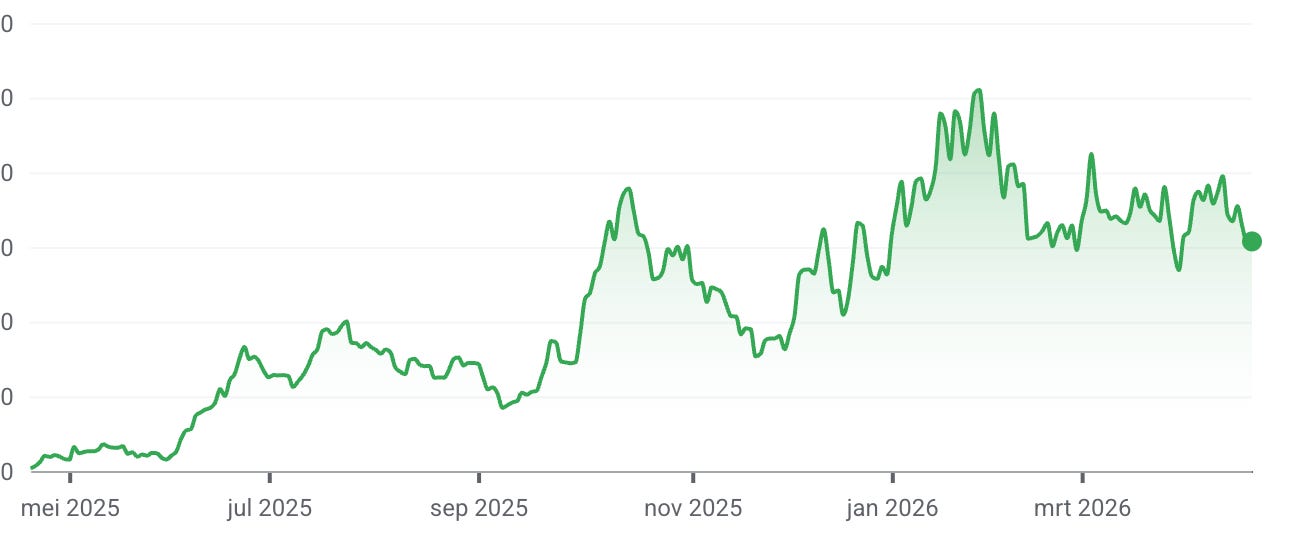

AST SpaceMobile has lost a satellite. Its stock is down nearly 50% from its all-time high. Analysts have a consensus "Hold" rating with an average price target implying significant downside. And yet the more I researched the reasons why AT&T and Verizon are betting billions on this company, the more I understood why I'm still holding. This is not a story about a satellite company. It's a story about who controls the infrastructure layer of the American wireless industry — and what happens if SpaceX wins that fight.

What they’re actually building

Roughly 40% of Earth’s land surface has zero mobile coverage. Billions of people carry smartphones that go dead beyond a city boundary. Starlink solves part of this — but requires dedicated hardware most people can’t access or afford.

AST’s answer is different. Their satellites connect directly to standard, unmodified smartphones using the mobile network operators’ own licensed terrestrial spectrum — like AT&T’s 850 MHz band. Your phone doesn’t know it’s talking to a satellite. It just works.

This has already been demonstrated — the first native voice-over-LTE calls and SMS messages over satellite using unmodified smartphones were completed on both AT&T’s and Verizon’s core networks through BlueBird 1-5. This is not a concept. The calls happened.

The question is whether they can build the constellation fast enough before the competition closes the gap.

The numbers

You cannot value this company on today’s earnings. You value it on what it looks like when operational.

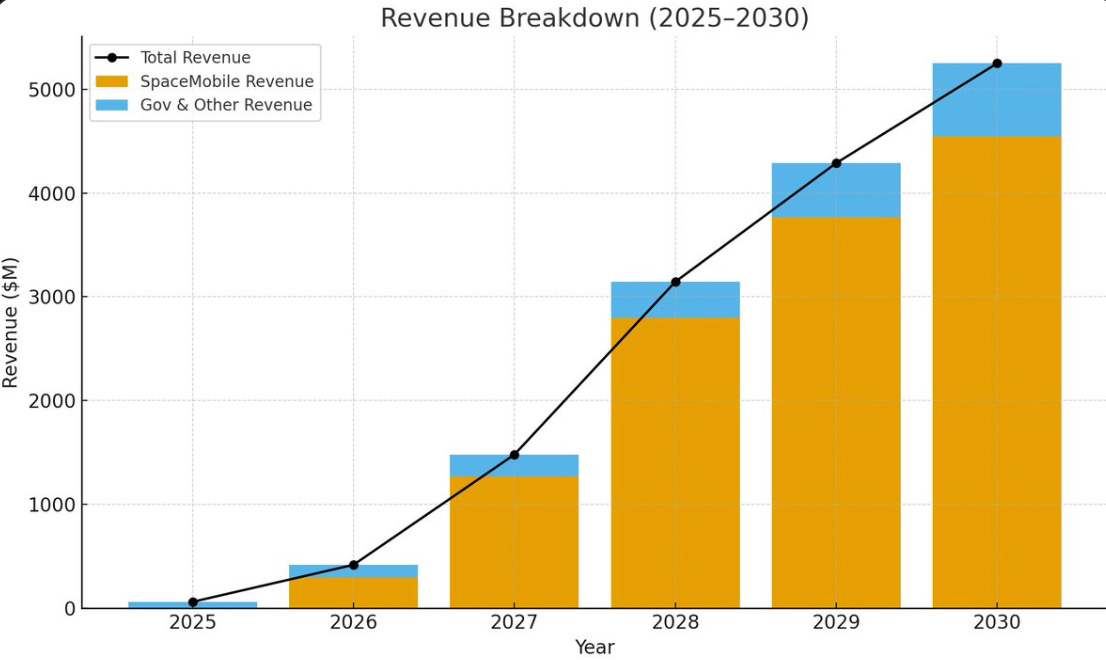

Full year 2025 revenue: $70.9 million — primarily government contracts and carrier milestone payments, not consumer service. Net loss: $341.9 million.

Management is guiding $150–200 million in 2026 revenue, and an ambitious $1 billion target for 2027. Going from $70 million to $1 billion in two years is a number that should make any investor pause. The company ended 2025 with $3.9 billion in liquidity — enough, management says, to fully fund the constellation through 2027. That’s the one number that makes this credible as a going concern.

The contracted backlog exceeds $1.2 billion, including a $175 million prepayment from stc Group and a definitive 10-year Verizon agreement. These aren’t letters of intent. Real money is attached.

Where the constellation stands — and the setback I can’t ignore

The target is 45–60 satellites in orbit by end of 2026, with launches every one to two months.

Block 2 BlueBird satellites are nearly 2,400 square feet in area — three times previous satellites, with ten times the capacity. That size is what allows a standard phone to connect without a specialised antenna. It’s the core engineering breakthrough.

But while finishing this research, BlueBird 7 was lost. I’m not going to gloss over it. The cost is covered by insurance, and BlueBirds 8–10 remain on track with delivery expected within approximately 30 days.

The timeline slipped. The business model didn’t. The AT&T and Verizon agreements have not changed.

The real reason AT&T and Verizon need ASTS to win

This is what most people miss — and it’s the part of this thesis I find most durable.

T-Mobile has an exclusivity deal with SpaceX’s Starlink for its direct-to-device offering, aggressively marketing free satellite connectivity to its customers while charging AT&T and Verizon subscribers $10 per month for the same service.

If SpaceX becomes the satellite infrastructure layer that the entire U.S. wireless industry depends on, Elon Musk gains structural leverage over every major American carrier. AT&T and Verizon need AST SpaceMobile to succeed — the alternative is handing SpaceX ownership of the infrastructure their combined customer bases will increasingly demand.

This isn’t just a commercial relationship. It’s a strategic necessity. AT&T has signed a binding six-year agreement and has four operational ground gateways live across the U.S. Verizon converted its $100 million strategic investment into a binding service contract. Active infrastructure commitments — not passive bets.

The revenue model is a 50/50 split between ASTS and the carrier, using the carrier’s existing billing and customer acquisition infrastructure. If this scales, the unit economics are extraordinary.

The competition — the honest bear case

Starlink has over 9,000 satellites in orbit, nine million customers, and is actively developing direct-to-device capability through T-Mobile and its EchoStar spectrum acquisition.

That development directly erodes AST’s differentiation.

The competitive window is not indefinitely open. Every delayed launch, SpaceX closes ground. The consensus analyst rating on ASTS is “Hold,” with average price targets implying meaningful downside, citing third-party launch dependency and capital-intensive constellation risk. I take that seriously.

Valuation — the genuinely hard part

The most bullish forecasts require approximately 386% average annual revenue growth to reach $2.1 billion by 2028.

Analyst price targets run from $41 to $145 — when the range of reasonable outcomes spans a factor of three, you’re making a directional bet on execution, not a traditional investment.

The honest framing: if the constellation deploys on schedule and AT&T/Verizon commercial services activate, the $1 billion 2027 target becomes plausible and the current valuation looks reasonable in retrospect. If deployment stalls and SpaceX closes the gap, the downside is severe.

Three things I’m watching

1. Constellation cadence.

One launch every one to two months through 2026. Every slip matters. I track each launch as a binary event. 🛰️

2. AT&T FirstNet activation.

Beta service for over 12 million U.S. first responders was targeted for the first half of 2026. This is the first real network revenue — not gateway sales, not government milestones. If this activates on schedule, it’s the inflection point the thesis needs.

3. Starlink’s D2D progress with T-Mobile.

The external variable I can’t control but watch most carefully. If T-Mobile achieves nationwide scale before ASTS reaches full constellation density, the competitive landscape changes fundamentally.

Honest conclusion

The technology works. The partners are real and strategically motivated. The market is enormous. But the execution window is narrow, the competition is SpaceX, and the valuation already prices in success that hasn’t happened yet.

I’m holding. I’m not sizing up until the deployment cadence holds for at least two consecutive quarters. BlueBird 7 was a reminder that in this business, things that look certain aren’t — and position sizing matters as much as thesis quality.

Still figuring this out. Watching every launch.

⚠️ This is not financial advice. I am not a licensed financial advisor. For educational purposes only. I hold a position in ASTS at time of writing. Do your own research.

If this gave you a different angle on ASTS — a restack helps this newsletter reach people doing real research. It means a lot.

Do you run a discord?