Rocket Lab's CEO Just Made a Move That Might Worry You.

Okay, here’s a sequence of events that made me stop scrolling.

Rocket Lab announces the biggest deal in its history - $8 billion to buy Iridium Communications. Stock pops 16% that day.

A week later: founder and CEO Peter Beck quietly files paperwork to sell 5 million of his own shares, roughly $465 million worth. Stock drops almost 10% in a single session.

Same company, same week, and on paper those two moves fight each other going all-in on a transformative deal, then cashing out half a billion days later. I spent the better part of a week pulling this apart.

You need to see this…

The Iridium Deal Is the Real Story Here

Rocket Lab is buying Iridium - the satellite comms company behind roughly 2.5 million subscribers across government, defense, aviation, and maritime.

→Iridium isn’t some speculative bolt-on:

- $8 billion enterprise value.

- $872 million in revenue in 2025

-$114 million of net income

→Rocket Lab on the other hand:

- $602 million in revenue

- lost $198 million.

So this isn’t Rocket Lab buying a shiny toy - it’s buying a profitable business roughly its own size. CFO Adam Spice called it “significantly accretive” to cash flow.

This makes sense strategically. Buying Iridium solves: constellation, spectrum, and a subscriber base.

What worries me is how it’s getting paid for: a $3.6 billion bridge loan from Deutsche Bank and a close that doesn’t happen until mid-2027…a long runway for the market to get nervous about the capital structure.

The Numbers That Actually Matter

Strip away the deal drama for a second, because the underlying quarter was genuinely strong. Not “beat by a penny” strong - actually strong.

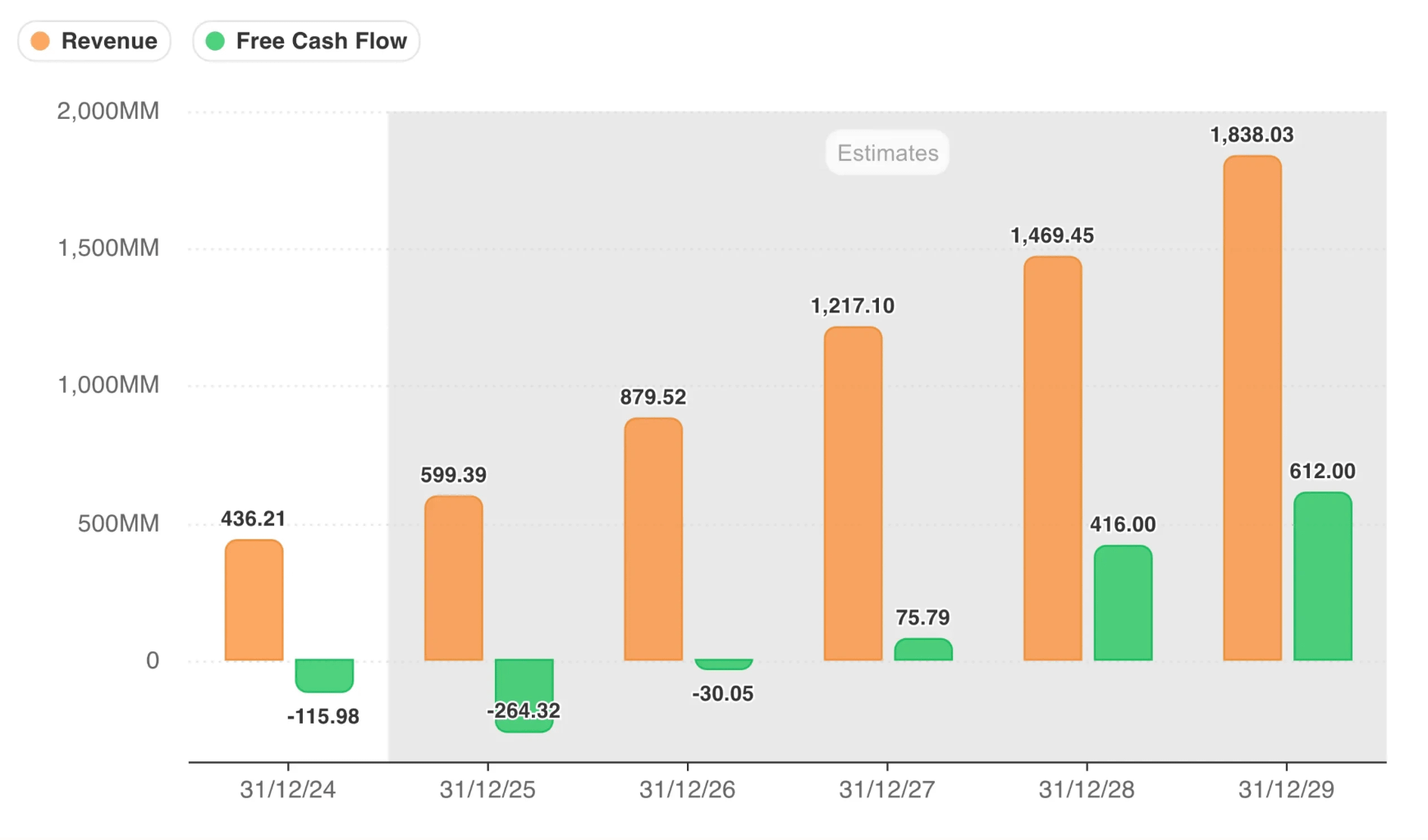

Revenue: $436M (2024) → $599M (2025), consistent revenue growth

Free cash flow: –$116M (2024) → –$264M 2025, worse despite 37% revenue growth

Space Systems - the satellite manufacturing side of the business - is now the bigger segment, at $136.7 million in quarterly revenue, growing faster than Launch

Backlog: $2.2 billion, up 108% year-over-year, up 20% from the prior quarter

They also signed the largest launch contract in company history - five Neutron missions plus three Electron flights for a confidential customer - plus a $190 million hypersonic testing deal with the DoD and new work with Anduril and Raytheon.

About 36% of the backlog converts to revenue in the next twelve months. That’s real visibility, not a promise about someday.

The Competitive Ground Just Shifted Too

Rocket Lab isn’t playing this alone, and that gets forgotten a lot.

SpaceX finally went public this year - roughly $86 billion raised, reportedly the largest IPO ever.

Now both sit side by side in the Nasdaq-100, compared line-item by every analyst on the Street.

Rocket Lab used to be “the closest thing to SpaceX you could actually buy.” That framing just got a lot more literal now that you can buy the real thing.

Worth knowing the rest of the peer group too. AST SpaceMobile is chasing direct-to-phone satellite connectivity and is still pre-revenue at scale.

Planet Labs monetizes Earth-imaging data instead of launch or hardware. None of them do what Rocket Lab does - build the rockets, build the satellites, and increasingly own the constellation too.

Blue Origin’s pushing its own satellite ambitions on top of all this. The sector’s consolidating fast, and this Iridium deal is part of that wave, not a standalone move.

The Part Almost Nobody’s Connecting: Agentic AI and Space Compute

Here’s the angle almost nobody writing about Rocket Lab ties together, and it’s worth understanding even loosely

I think it matters more over the next decade than most people give it credit for.

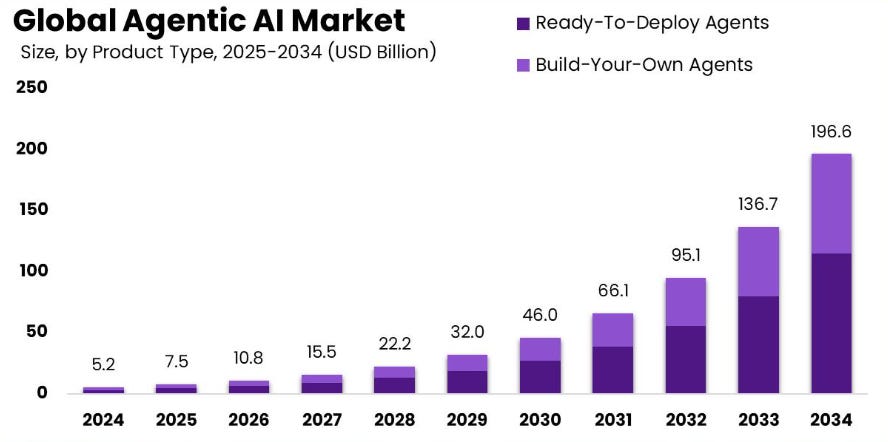

Agentic AI - software that plans and takes action across tools mostly on its own is one of the fastest-growing corners of tech right now.

Estimates bounce around, but most put the global market around $9-11 billion in 2026, growing north of 40% a year, with some forecasts near $66 billion by 2031.

Gartner expects 40% of enterprise apps to carry task-specific agents by year-end, up from under 5% last year, and puts overall global AI spending near $2.5 trillion in 2026. Whatever the precise number, nothing else in enterprise software is scaling this fast

.

All of that compute has to run somewhere, and terrestrial data centers are hitting real walls - land, power, grid queues stretching past five years in places like Northern Virginia.

So a handful of serious players are chasing an idea that sounded absurd two years ago: put the data centers in orbit. Google’s Project Suncatcher just passed radiation testing simulating five years in space.

Starcloud, a Seattle startup, already ran an Nvidia chip in orbit and trained a language model up there, hitting a $1.1 billion valuation seventeen months after leaving Y Combinator. SpaceX has filed with regulators for a constellation of up to a million satellites built around distributed compute.

Here’s where Rocket Lab fits without being one of these companies itself: every one of these projects needs satellites built and launched, over and over, at a pace the industry’s never sustained before.

Rocket Lab’s Space Systems arm already builds that hardware, and its launch business benefits from a growing pipeline of satellite launches no matter which orbital-compute bet wins.

Its Iridium acquisition adds direct-to-device connectivity in that same infrastructure layer.

About That Insider Sale

That’s the whole point of these plans: schedule the sale in advance so nobody can call it trading on news you just announced.

Five million shares is under 1% of shares outstanding. Trailing 90-day insider selling - almost all Beck… adds up to roughly $896 million.

Which sounds alarming until you remember the stock’s up over 100% in a year and Beck’s entire net worth has sat in one ticker for two decades.

At some point a founder’s allowed to buy a house.

Doesn’t mean I’d wave it away completely. A founder pulling half a billion off the table the same week his company takes on billions in new debt is worth flagging. I just don’t think it justifies an 18% two-day drawdown on its own. The real risk is dilution.

What I’m Actually Watching From Here

Rocket Lab went from a scrappy small-launch company to a business betting everything on becoming a genuine rival to SpaceX. More moving parts. More debt.

None of that’s a verdict, good or bad - it’s just the actual shape of the bet, as best as I can piece it together from what’s public right now.

I am not actively buying Rocket Lab.

⚠️ This reflects my own research as of July 14, 2026, cross-checked against primary sources and filings where I could find them. Shared for educational purposes only, in line with MiFID II and FSMA guidelines nothing here is personalized investment advice, and none of it is a recommendation to buy, sell, or hold anything. Do your own research, and talk to a licensed advisor before making any investment decisions.

Interesting analysis. I never worry too much when I see insiders selling, because it could be for one of a million reasons. The timing was a little sketchy, I’ll agree there. Now when insiders buy, they do so for one reason only.

Good sights, thanks for the sharing. I'm also not too worried about the CEO sell as insiders sell for a variety of reasons.